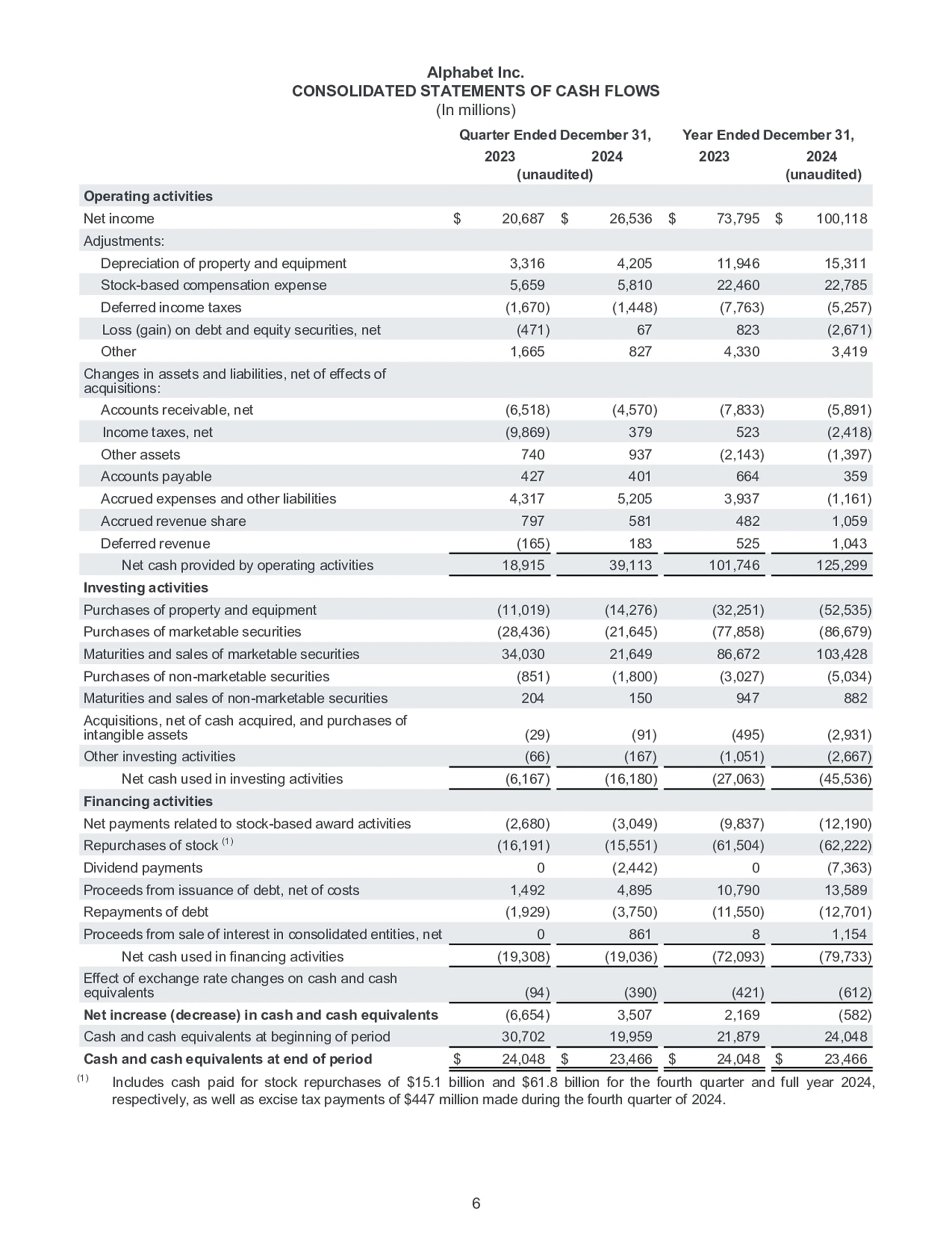

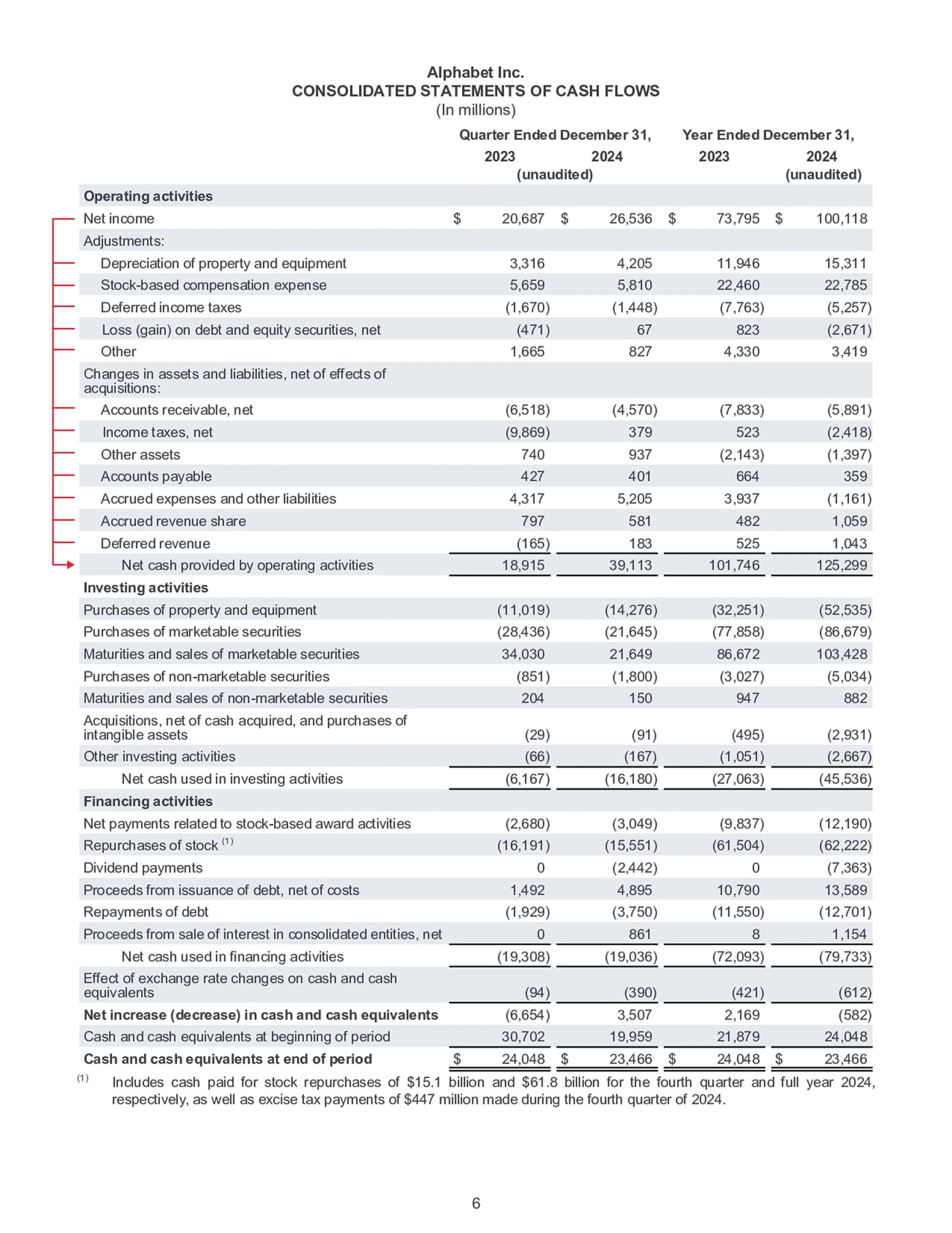

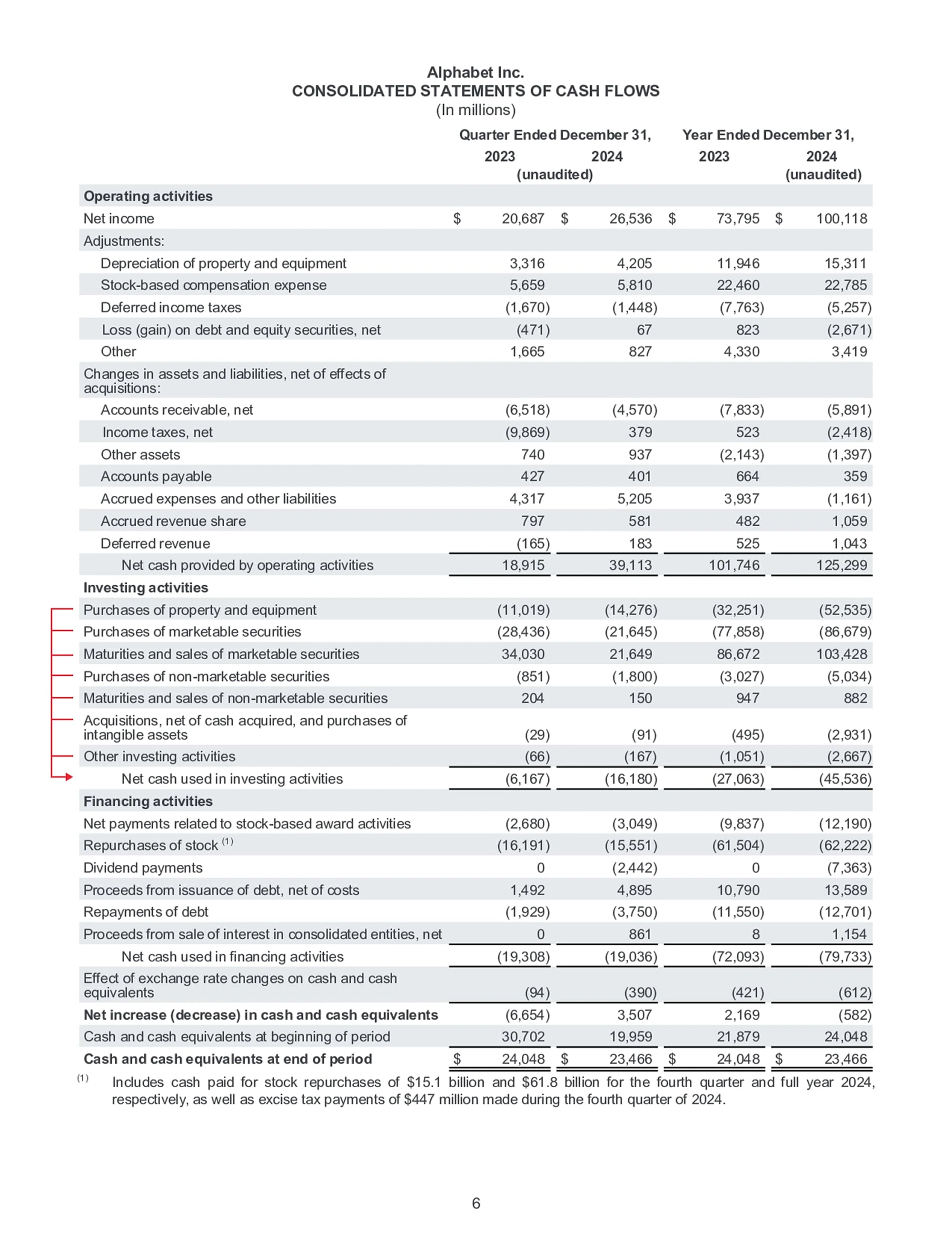

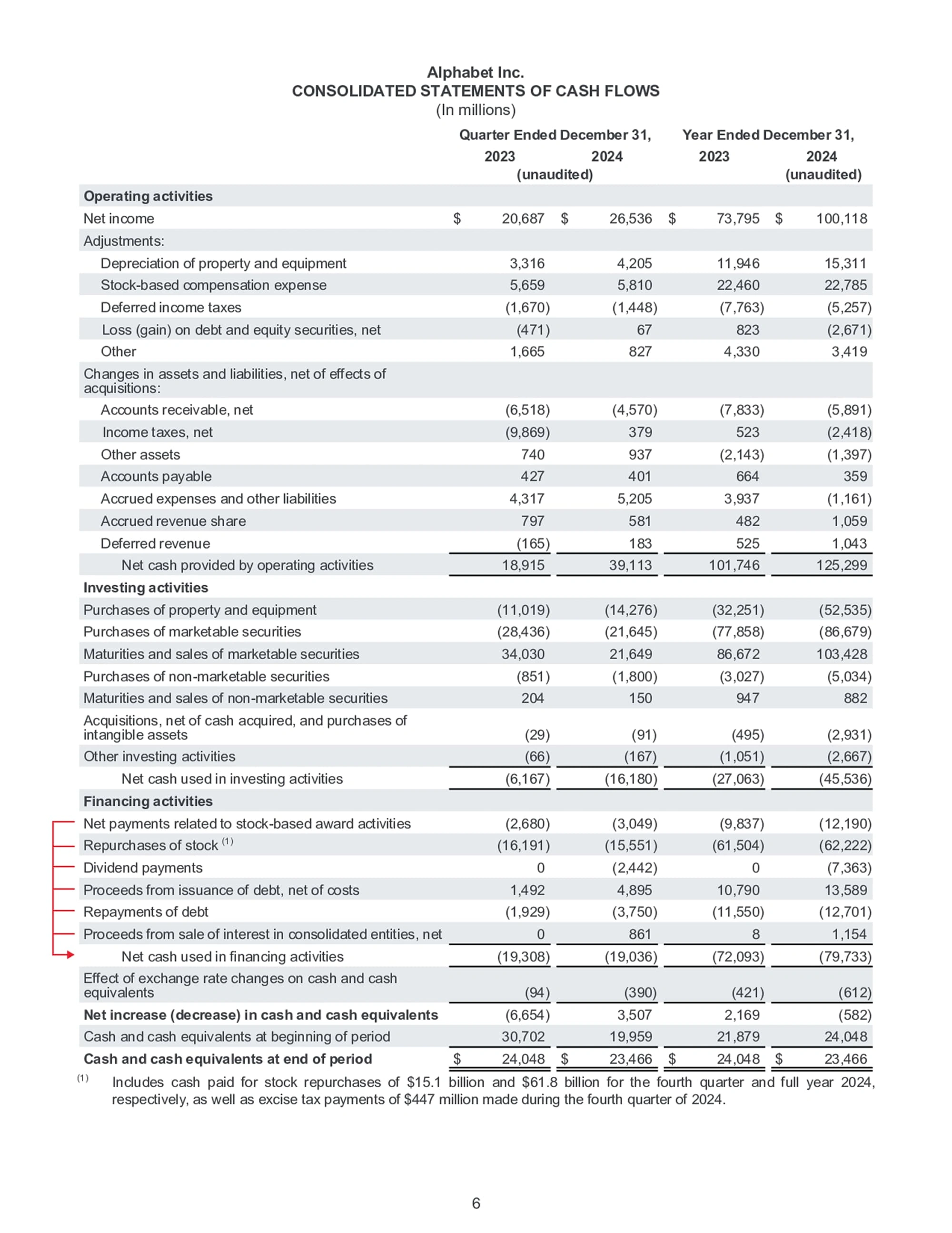

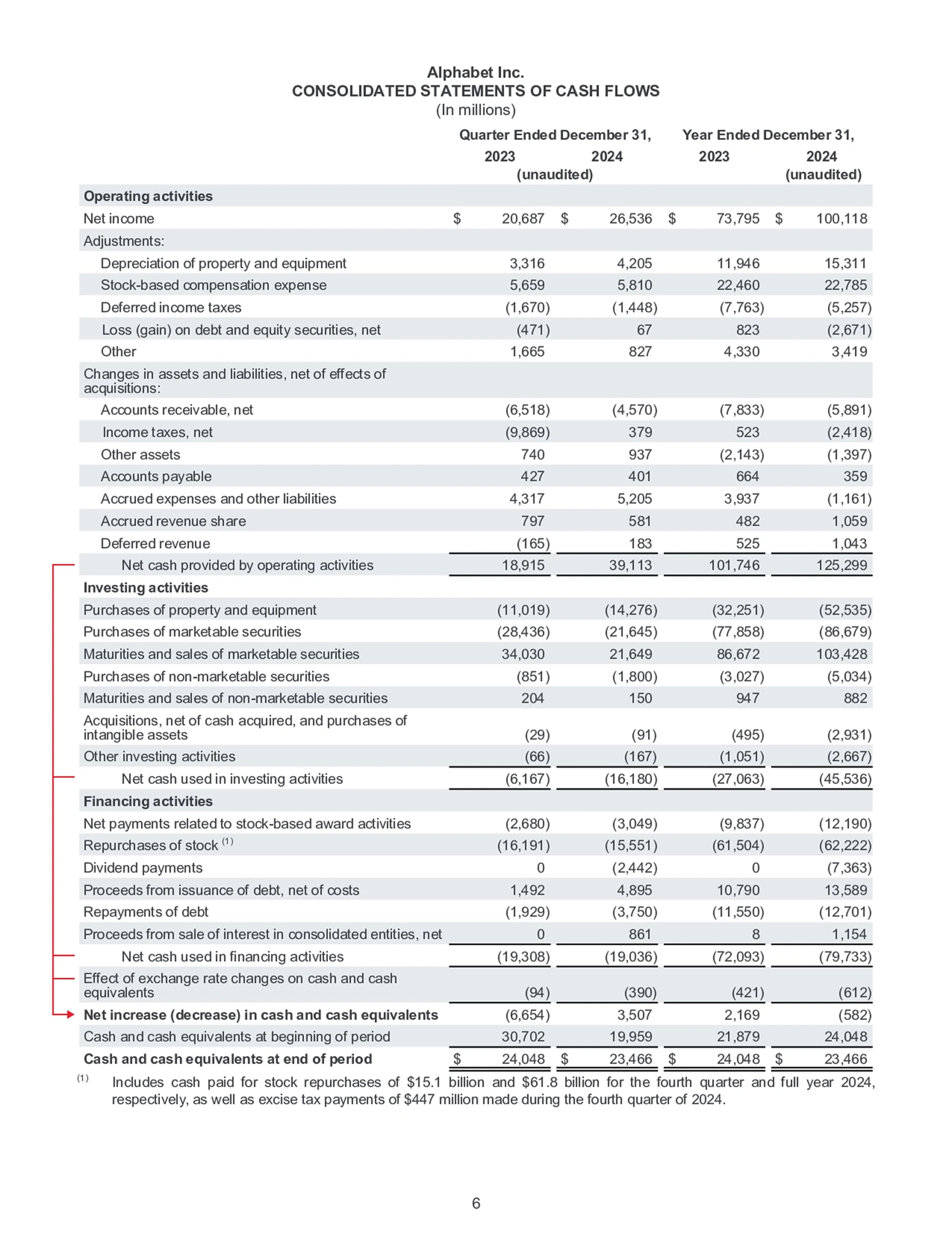

Before we dive in, you might want to take a look at this simplified Alphabet 2024 Q4 financial statement. This will at least give you a basic idea of what one looks like. We'll be using this simplified report for our examples later on.

Of the three main financial statements, the Balance Sheet lists 'what a company owns and owes,' and the Income Statement tells us 'how much profit it made on paper.'

But the Cash Flow Statement... that's the one that shows how much actual cash the company put in its pocket.

When the market is getting yanked around by short-term numbers and emotions, we need to go back to cash flow. By focusing on the actual cash a company brings in, we can identify its "real value" and find our margin of safety for holding on long-term. This is how we find the most solid basis for an investment.

What is the Cash Flow ?

The Cash Flow Statement is a financial report that records "how much actual cash" a company brought in and spent during an accounting period. Cash flow is broken down into three main activities—Operating, Investing, and Financing—which lets investors see exactly where the cash came from and where it went.

So, let's review this one more time:

- The Balance Sheet is a snapshot of the company's "assets and liabilities" at a specific point in time. It analyzes what the company has, what it owes, and what its net worth is.

- The Income Statement records how much profit a company made over a period of time, but conceptually, this is more like its "on-paper performance."

- The Cash Flow records how much cash the company generated during that same period. It shows the actual money that came in and the money that went out. It's much harder to "cook the books" with cash. You either earned the cash, or you didn't.

Just because a company has "sales on the books" doesn't mean the cash has actually come in. Maybe a customer is paying late, or maybe that "profit" is really just sitting in inventory. That's why you must confirm that the business's operations have a stable, consistent flow of cash coming in. The Cash Flow Statement is the report that tracks exactly that.

Cash Flow from Operating Activities

This is the cash generated from a company's day-to-day core business. It's the most important item on the cash flow statement and the most direct indicator of a company's money-making ability.

After you subtract the capital expenditures needed to maintain the business (and this doesn't include new investments, debt payments, or dividends), what's left is the cash that truly belongs to the shareholders.

Its main components are:

- Net Income: Taking the "net income" from the income statement and using it as the starting point to get to a cash number.

- Adjustments: Adding back non-cash expenses, like depreciation and amortization.

- Changes in Working Capital: This includes changes in accounts receivable, inventory, prepaid expenses, accounts payable, and accrued expenses.

- Other operating cash items: Things like provisions for losses, deferred income tax, and minority interest cash flow.

For value investors, a high and stable operating cash flow means a few great things:

- It shows the cash is real. The company can keep generating actual cash, even when the market is volatile or when it gets hit with one-time charges.

- It gives you more certainty in its intrinsic value. This makes your Discounted Cash Flow (DCF) models much more reliable.

- It proves the "moat" is strong. Healthy cash flow is what pays for the R&D, marketing, and stock buybacks that keep a company's competitive advantage going strong for years.

Cash Flow from Investing Activities

This section covers the capital expenditures a company makes for its future growth and to build its moat, as well as any cash it gets from selling off assets. These are typically one-time expenses or inflows.

Investing activities are key to understanding a company's long-term strategy and how it allocates capital. This is money spent on things like buying new hardware or expanding production capacity—all part of its plan for the future, like widening that moat. But at the same time, this can eat up a lot of cash. So, you have to look closely at its past investments and see if they've actually paid off.

Key Items

- Capital expenditures (CapEx): This is money spent to maintain or expand its operations, like buying property, plant, and equipment (PP&E) or investing in R&D.

- External investments and M&A (Mergers & Acquisitions): This is the cash that flows in or out from buying subsidiaries, making equity investments, or selling those investments.

- Acquiring or selling other capital assets: This includes things like buying or selling real estate or transferring long-term equity.

When is a large outflow a good thing?

- It's good when the company has a clear and sustainable competitive advantage, and it's spending that capital to make its moat even wider—like opening new production lines or acquiring a key supplier.

- It's the best-case scenario if the investment is set to deliver clear, significant growth in future cash flow, and the company's current operating cash flow can cover the cost of the investment. That's healthy expansion.

How can you spot weakening growth?

- If the company invests money year after year, but its operating cash flow stays flat, or if its capex starts eating up a huge chunk (say, over 50%) of its operating cash flow, it might mean its "moat" isn't being used effectively.

- If you see large-scale asset sales, you need to be cautious. It could be a red flag that they're being forced to sell things off because the business is being managed poorly.

An Industry and Cycle Perspective

- The need for CapEx varies wildly by industry. Manufacturing and heavy-asset industries naturally have high investment needs, while software or service companies will have much lower ones.

- When you're judging if an investment is "reasonable," you must consider the state of the industry and where the company is in its life cycle. Don't just look at the dollar amount and make a snap judgment.

Cash Flow from Financing Activities

This section records the company's "fundraising or repayments." It's used to judge if the company's capital structure is healthy and to understand its policy on shareholder returns.

Usually, there's nothing very creative about financing cash flow; it doesn't change much. You just need to watch and make sure the company isn't doing anything crazy with its capital. It's mainly made up of the following:

- Issuing and Repaying Debt: Cash inflow means taking on new debt; cash outflow means paying off debt.

- Paying Dividends: This is a core part of investing. The company takes its profits and gives some back to you as a dividend.

- Treasury stock: When the company thinks its stock is undervalued, it buys back its own shares. This reduces the number of shares out in the market, which helps increase the value of every remaining share.

Free Cash Flow vs. Net Cash Flow

Once you understand what Operating, Investing, and Financing cash flows mean, the next step is to calculate Free Cash Flow and Net Cash Flow. By subtracting the investing and financing cash flows from the operating cash flow, you can track whether the company is overspending each year.

- Free Cash Flow = Operating Cash Flow + Investing Cash Flow

- Net Cash Flow = Operating Cash Flow + Investing Cash Flow + Financing Cash Flow

Whether you're looking at free cash flow or net cash flow, the result you want to see is a "positive and stable number." This means the company has leftover cash every year to pay dividends, buy back stock, or invest even more. Cash-generating machines, like Apple, have looked like this for years.

Typically, value investors pay more attention to Free Cash Flow. It checks if the cash the company generates on its own is enough to cover its spending on future growth. Does that mean Net Cash Flow isn't important? Not really, it's just that value investors prefer to look at "Financing Cash Flow" separately, because we'd rather pick companies that already have a healthy capital structure to begin with.

The Importance of Free Cash Flow

When a company has excellent free cash flow, it's like having a super-strong margin of safety. It doesn't need to rely too much on outside financing, so it stays resilient even when the market is down or interest rates go up.

When free cash flow is strong enough, the company has the power to call its own shots. It has the choice to pay back shareholders, expand into new business lines, or just pile up a cash reserve—it can pick whatever option will create the most long-term value.

Judging Its Stability

Look at the free cash flow over multiple periods (try to pull at least 10 years of data). If it shows stable, long-term growth or at least stays reliably steady, it's a sign of a healthy business model.

If it's jumping all over the place (high one year, low the next), you can probably just ignore the company. But, if you insist on tracking it, you need to dig deeper and find out why. Start by looking for clues in the financial statements, then check the news archives to see what was happening at that time.

What we love to see are companies with stable, growing cash flow—the kind that just keep printing cash like a machine.

Predicting the Future? The Mindset Value Investors Need to Have

A lot of people probably rush online looking for some complex formula to predict future cash flow. I need to get one important concept in your head first: the business world changes every single day, and there is no such thing as a 100% accurate formula.

So, does that mean we just don't make predictions? No! We still have to!

But we don't make "precise predictions." We make "conservative estimates." And we only do it for things that are within our circle of competence. This is exactly where the core principles of value investing come into play.

- We focus on companies whose business models are stable and relatively easy to predict, with a strong track record of cash flow. If a company's next ten years of cash flow feel like a total mystery to you, it's probably outside your circle of competence.

- Precisely because we know our estimates won't be perfect, we demand a "margin of safety." That's the buffer zone between the price we pay and the value we've estimated. It's what protects us when we're wrong.

Instead of wasting your time trying to find the perfect formula, you should spend your time looking for "predictable" and "great" businesses. When you find a company like that, you'll discover that estimating its future becomes a whole lot simpler, and you'll have a lot more confidence in it.

Let's Walk Through a Real Cash Flow Statement

Compared to the Income Statement, the Cash Flow Statement is a lot more straightforward.

This is the report you use to check a company's ability to generate cash and to see if that cash is enough to cover its spending. It's what validates a company's real money-making power.

The Structure of the Cash Flow Statement

As mentioned, the Cash Flow Statement is broken down into three main categories: Operating, Investing, and Financing.

- Operating tracks the cash generated from the main business.

- Investing tracks items like securities, property, and equipment.

- Financing explains the company's capital situation (like debt and equity).

The Operating activities section is where you calculate the net cash from operations. It's the total you get after combining Net income with all the other operating-related items.

Numbers in parentheses mean it's a negative number.

For the Investing activities section, you just take all the items from "Purchases of property and equipment" down to "Other investing activities". Add those numbers up, and that's your net cash from investing.

The Financing activities section is the same deal. It's all the items from "Net payments related to stock-based award activities" down to "Proceeds from sale of interest in consolidated entities, net." Add all those numbers up, and that's your net cash from financing.

Finally, you add up the net totals for Operating, Investing, and Financing cash. Then, you add in the number for the "Effect of exchange rate changes on cash and cash equivalents", and that gives you your "Net increase (decrease) in cash and cash equivalents".

The lines at the bottom, "Cash and cash equivalents at beginning of period" and "Cash and cash equivalents at end of period," just tell you the total cash balance on the books when the period started and when it ended.

Just a quick note: I mentioned earlier that value investors really care about free cash flow. You won't actually find that number on the cash flow statement itself. It's something you have to calculate on your own (though, honestly, these days all the major financial or stock investing websites will calculate it for you).

Terms You'll See on the Cash Flow Statement

- Operating activities: Cash flow generated from the company's core business.

- Net income: This is the starting point for calculating operating cash flow. The number comes straight from the net profit on the Income Statement.

- Adjustments: Since net income is calculated on an accrual basis (not a cash-in, cash-out basis), this section is all about backing out all the items that don't actually affect cash, to get the number back to a "cash" basis.

- Depreciation of property and equipment: Depreciation gets counted as an expense on the income statement (which lowers net profit), but it's not a real cash payment. You didn't actually write a check for it. So, you have to add it back here to get the true cash amount.

- Stock-based compensation expense: This is when the company gives employees stock or options as part of their pay. It's an expense that lowers net profit, but it's not a cash payout.

- Deferred income taxes: This is due to timing differences between accounting rules and tax laws. The change here affects the tax expense on the income statement, but it doesn't represent the actual cash paid in taxes for the period.

- Loss (gain) on debt and equity securities, net: This is the profit or loss from selling investments. Since that money belongs in the "Investing activities" section, you have to back it out of the Operating section here.

- Other: Other profit or loss items that don't affect cash, like an asset write-down (impairment). The principle is the same as depreciation.

- Changes in assets and liabilities, net of effects of acquisitions: This means the following lines are all operating-related asset changes, but they've excluded any impact from acquisitions. The cash impact from an acquisition is recorded under Investing activities.

- Net cash provided by operating activities: After all those adjustments to net income, this is the final number. It shows the actual net cash the company's core business generated (an inflow) or spent (an outflow).

- Investing activities: Cash flow from buying and selling long-term assets and other investments.

- Purchases of property and equipment: Cash paid to buy fixed assets (like property, plant, and equipment) to expand or maintain operations. This is a cash outflow.

- Purchases of marketable securities: The company buying easy-to-sell securities like stocks and bonds as an investment. This is a cash outflow.

- Maturities and sales of marketable securities: Cash the company got from selling its marketable securities or from a security (like a bond) maturing and getting the principal back. This is a cash inflow.

- Purchases of non-marketable securities: Buying securities that aren't on a public market and are hard to sell (like stock in a private company). This is a cash outflow.

- Maturities and sales of non-marketable securities: Cash received from selling or cashing in those non-marketable securities. This is a cash inflow.

- Acquisitions, net of cash acquired, and purchases of intangible assets: This is the cash outflow from buying other companies or intangible assets (like patents or trademarks). "Net of cash acquired" means the total price paid minus the cash that was on the acquired company's books.

- Net cash used in investing activities: The net total of all cash inflows and outflows from investing. For a growing company, this is typically a negative number (a net outflow), showing that the company is actively investing in its future.

- Financing activities: Cash flow from activities that change the company's equity (ownership) and debt levels.

- Net payments related to stock-based award activities: This relates to cash movements for employee stock plans—like the company buying back its own stock to cover awards, or cash coming in from employees exercising their options. "Net payments" here just means the cash out was more than the cash in.

- Repurchases of stock: Cash spent by the company to buy back its own stock from the open market. This is a cash outflow.

- Dividend payments: The cash the company paid out to its shareholders. This is a cash outflow.

- Proceeds from issuance of debt, net of costs: The net cash the company received from raising money by taking on new debt (like bank loans or bonds). This is a cash inflow.

- Repayments of debt: Cash the company spent to pay down the principal on its loans or bonds. This is a cash outflow.

- Proceeds from sale of interest in consolidated entities, net: Cash the company received from selling off a portion of one of its subsidiaries (while still keeping control). This is considered an equity transaction with external shareholders.

- Net cash used in financing activities: The net total of all cash inflows and outflows from financing.

- Effect of exchange rate changes on cash and cash equivalents: If the company holds cash in foreign currencies, this line adjusts for changes in that cash's value simply due to fluctuating exchange rates.

- Net increase (decrease) in cash and cash equivalents: This is the grand total. You add up the net cash from operating, investing, and financing, plus that exchange rate effect, to get the total net change in the company's cash for the period.

- Cash and cash equivalents at beginning of period: The cash balance at the end of the last period, which is the cash they started this period with.

- Cash and cash equivalents at end of period: The starting balance plus this period's net change. This is the total cash and cash equivalents the company has at the end of this period. This number should match the "Cash and cash equivalents" line on the Balance Sheet.

The Cash Flow Statement is a Key to Judging a Company's Health

Warren Buffett's famous line is, "Price is what you pay. Value is what you get". The Cash Flow Statement is the single best tool we have for seeing that real value.

Unlike the "on-paper profits" on the Income Statement, the Cash Flow Statement reveals the actual, hard cash moving in and out of a company. A business might be able to make its profits look good in the short term, but its ability to consistently generate cash cannot be faked. This is why, for value investors, the Cash Flow Statement is such a critical report for judging a company's true health.

At this point, you've read through the "Big Three" financial statements: the Balance Sheet, the Income Statement, and the Cash Flow Statement. You now have a basic idea of how to use these reports to get to know a company and understand the most fundamental tools of value investing.

Next up, we'll start diving into the various financial ratios. These ratios are simply formulas built from the data in these three statements. They're designed to help you more easily see and understand the numbers you really need to be paying attention to.